Address

304 North Cardinal St.

Dorchester Center, MA 02124

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

Address

304 North Cardinal St.

Dorchester Center, MA 02124

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

Have you ever wondered how savvy investors manage to keep more of their earnings away from the taxman? In the complex world of investing, understanding the nuances of taxes can significantly enhance your financial strategy and net gains. This comprehensive guide will navigate through essential tax tips every investor should know, ensuring you’re equipped to make more informed decisions and potentially boost your investment income.

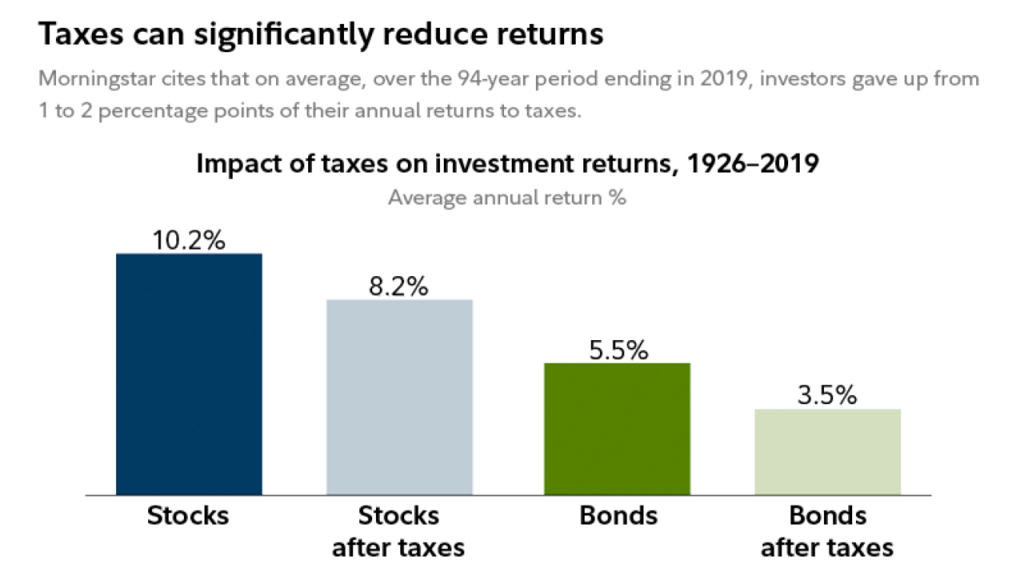

In the ever-evolving landscape of finance, tax laws frequently change, impacting how investments are taxed and what strategies are most effective for saving money. With the IRS scrutinizing investment gains more closely, it’s paramount for investors to stay informed and agile. A significant number of investors may be paying more in taxes than necessary, due to a lack of knowledge about tax-efficient investing strategies.

Tax brackets determine the rate at which your income, including investment gains, is taxed. Understanding these brackets is crucial for effective tax planning. For example, long-term capital gains are taxed at preferential rates compared to ordinary income, which can significantly impact investment decisions. By knowing your tax bracket, you can strategize around the types of investments you make and the accounts you use. Investing through tax-efficient vehicles like Roth IRAs or 401(k)s can offer tax-free growth or tax deferral, thereby reducing your taxable income. Additionally, diversifying your portfolio to include a mix of tax-free (such as municipal bonds), tax-deferred (like traditional IRAs), and taxable investments ensures a more balanced approach to managing tax liabilities. This strategy not only helps in optimizing returns but also in managing cash flows more effectively, as the tax impact on withdrawals can vary significantly.

Capital gains and loss harvesting is a strategic approach to minimize taxes on investment profits. By selling investments that have lost value, investors can offset the capital gains realized from selling profitable investments. This strategy is particularly effective in years where market volatility results in both gains and losses within a portfolio. Not only does loss harvesting reduce your immediate tax liability, but it also offers an opportunity to reinvest the proceeds into investments with potentially higher returns. However, it’s crucial to be aware of the wash-sale rule, which prohibits claiming a tax deduction for a security sold in a loss-harvesting move if a substantially identical security is purchased within 30 days before or after the sale. Properly executed, this strategy can enhance the after-tax return of your investment portfolio.

Contributing to tax-advantaged accounts like IRAs, 401(k)s, and HSAs is a cornerstone strategy for reducing taxable income. These accounts offer different benefits, such as tax-free growth in the case of Roth IRAs and HSAs, or tax-deferred growth with traditional IRAs and 401(k)s. By maximizing contributions, investors can significantly lower their current taxable income while preparing for future financial needs. For example, funds in a 401(k) or traditional IRA grow tax-deferred until withdrawal, at which point they are taxed as ordinary income. In contrast, Roth accounts require contributions to be made with after-tax dollars, but withdrawals in retirement are tax-free. Choosing the right mix of these accounts can depend on your current tax bracket, expected tax bracket in retirement, and specific financial goals.

Charitable giving can be a powerful tax-saving strategy for investors. Donating appreciated securities, such as stocks or mutual funds, directly to a charity allows investors to avoid paying capital gains taxes on the appreciation, while still qualifying for a tax deduction equal to the full market value of the donated asset. This strategy is particularly advantageous for securities that have significantly increased in value since their purchase. It not only benefits the charity but also allows the donor to reallocate resources within their portfolio without the tax burden of capital gains. Smart charitable giving requires careful planning to ensure that the chosen charity is equipped to receive such gifts and that the donation aligns with the investor’s overall financial and philanthropic goals.

Mutual fund distributions, whether from capital gains, dividends, or interest, can impact an investor’s tax liability. Funds typically distribute capital gains at the end of the year, and these distributions are taxable to the fund’s shareholders, regardless of whether the shares have been sold at a gain or loss. Being mindful of a fund’s distribution schedule can help investors avoid buying into a mutual fund shortly before a distribution, which would result in a tax liability without the benefit of the full economic gain. Instead, timing purchases after distributions can help minimize unnecessary tax exposure. Additionally, considering funds with low turnover rates can help reduce the frequency and size of taxable distributions, as these funds tend to generate fewer capital gains.

Stay Informed: Regularly updating your knowledge of tax laws and regulations ensures that your investment strategies remain aligned with the latest tax-saving opportunities, safeguarding against overlooked deductions or credits.

Utilize Tax-Loss Harvesting: Implementing tax-loss harvesting can significantly reduce your tax liability on capital gains by offsetting losses against gains, making it a crucial strategy during the annual tax planning process.

Maximize Contributions to Tax-Advantaged Accounts: Increasing your contributions to accounts like IRAs and 401(k)s can lower your taxable income while bolstering your retirement savings with tax-efficient growth.

Consider the Tax Impact Before Transactions: Evaluating the potential tax consequences of buying or selling investments can prevent unexpected tax bills and influence timing decisions for better financial outcomes.

Consult with a Tax Professional: Engaging a tax expert can provide customized advice that aligns with your unique financial situation, ensuring that your investment decisions are both tax-efficient and conducive to achieving your long-term financial goals.

By incorporating these essential tax tips into your investment strategy, you can not only comply with tax laws but also significantly enhance your financial outcomes. Remember, the key to tax-efficient investing is staying informed and proactive about your tax planning. Share your thoughts or strategies in the comments below, and don’t forget to check out our related posts for more financial insights.